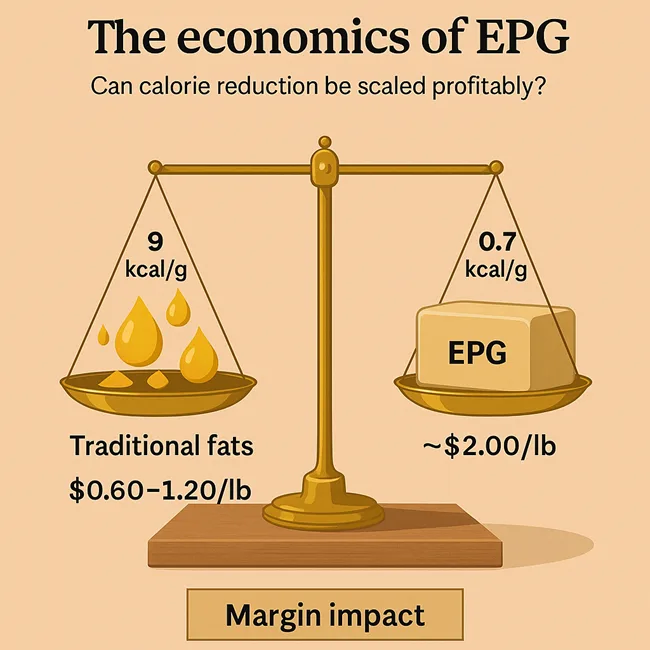

What is EPG and how much does it cost compared with traditional fats?

Engineered from rapeseed or other plant oils, EPG (esterified propoxylated glycerol) delivers fat-like texture but is minimally absorbed—providing just 0.7 kcal/gram versus 9 kcal/gram in ordinary fat. Developed by Epogee, the ingredient is being reformulated into recipes under mounting regulatory and health pressure. Early-stage production cost estimates place EPG at approximately $2 per pound. In comparison, commodity fats such as canola or palm oil typically range from $0.60 to $1.20 per pound depending on seasonality, while MCT oil trades at $3 to $5 per pound.

Though EPG’s cost premium averages about $1.20 per pound over conventional fats, the ingredient’s ability to reduce per-serving calorie loads by 25% to 90%—and its ability to maintain sensory quality—positions it as a uniquely viable reformulation solution.

How does EPG impact gross margins when used in reformulated products?

Ingredient cost directly impacts gross margin in food manufacturing, particularly in high-volume packaged foods. Fortunately, EPG performs as a drop-in fat alternative across bakery, frozen, and snack applications, meaning minimal investment in retooling or processing. A reformulation example replacing 5 out of 10 pounds of traditional fat with EPG adds around $6 in cost per batch. Scaled to 500 batches per month, this amounts to a $3,000 increase.

However, if calorie reduction enables a product to be positioned as lower-calorie, HFSS-compliant, or eligible for school procurement or premium retail placement, the cost can be offset. Data suggests that even a 10–15 cent price premium per retail unit can recapture the added cost if taste and volume remain stable—especially in macro-conscious categories like bars and functional desserts.

Can economies of scale bring EPG costs down?

Industry experts believe EPG’s pricing could decline as volume grows. The global market for oil and fat substitutes reached $2.2 billion in 2022 and is expected to grow to $3.4 billion by 2031. If demand continues to scale across categories, input costs for base materials like glycerin and processing throughput for Epogee could improve, potentially pushing EPG costs closer to $1.50 per pound.

This becomes transformative for private-label and national brands that depend on high-volume unit economics. As larger contracts are negotiated and more brands reformulate at scale, ingredient pricing is expected to compress—mirroring past ingredient adoption curves seen with pea protein, allulose, or MCT oil.

How are private-label and institutional buyers responding to EPG?

Private-label food producers supplying retail chains and institutional foodservice providers are showing strong early interest in EPG. These manufacturers are often tasked with balancing price-sensitive consumers with compliance to macro thresholds or school meal standards. Because EPG integrates easily and doesn’t affect mouthfeel, it allows reformulations that can lower calories while preserving sensory expectations.

However, recent legal action underscores supply fragility. In June 2025, brands including Own Your Hunger and Lighten Up Foods sued David Protein—the startup that acquired Epogee in 2025—alleging anticompetitive access restriction to EPG. The plaintiffs claim over $450,000 in R&D losses and disrupted commercialization plans. While still under litigation, the case has prompted industry stakeholders to demand transparency in EPG’s distribution, particularly as smaller players rely on equal access to deliver compliant, healthier foods affordably.

What regulatory incentives support EPG adoption by large manufacturers?

Global regulatory trends are accelerating food reformulation. In the United Kingdom, HFSS regulations prevent non-compliant foods from being promoted in prime retail locations. Mexico’s NOM-051 imposes front-of-pack warnings for products with excess calories, saturated fat, or sugar. The United States is moving toward front-of-pack calorie labeling and tightening rules around school meal compliance.

For multinational food brands, avoiding regulatory penalties, marketing restrictions, or lost retail shelf positioning is increasingly tied to calorie reduction. EPG enables calorie drops without flavor degradation or radical reformulation, allowing CPG majors to stay compliant and consumer-friendly simultaneously. Analysts suggest the cost of reformulating with EPG is often less than the long-term brand and placement losses incurred by regulatory non-compliance.

What are experts and investors saying about EPG and its markets?

Ingredient-focused investors view EPG as part of a new wave of commercially viable health-forward inputs that combine performance with compliance and margin flexibility. Epogee’s parent firm, Eastern Polymer Group PCL, reported a 6.7% pretax margin and 3.7% free cash flow margin in Q1 FY2025, despite ongoing R&D and integration costs.

Institutional investors forecast these margins could improve to the 8–12% range within 18–24 months, driven by capacity expansion, foodservice deals, and international licensing. While still a mid-stage ingredient innovation, EPG is now well beyond pilot use, entering structured R&D pipelines at multiple food conglomerates. Should lawsuits resolve and licensing widen, analysts expect heightened M&A activity around scalable, GRAS-compliant, clean-label ingredients like EPG.

What could disrupt EPG’s commercial trajectory?

EPG’s future is not guaranteed. Overcentralization of supply, as illustrated by the David lawsuit, may spook smaller brands or trigger regulatory review. Ingredient cost volatility, geopolitical trade issues affecting glycerin feedstock, or emerging competition from fermentation-derived or novel structured fats could cut into its market share.

Moreover, while EPG is GRAS-approved in the United States, its use outside North America still faces novel food authorization hurdles, particularly in the EU, where it must undergo EFSA review. Marketing strategy also matters—if consumers perceive EPG as too synthetic or associate it with failed fat replacers of the past, brand trust could be affected. However, most early adopters have successfully framed EPG usage in the context of calorie transparency and macro-conscious formulation, mitigating these risks.

What’s the long-term outlook for EPG in food reformulation?

The long-term outlook for EPG in global food reformulation is increasingly promising, especially as public health mandates, consumer awareness, and retailer expectations converge on the need for reduced-calorie food systems. If ingredient supply chains remain open and pricing improves through scale, EPG is well positioned to become a foundational platform ingredient in the next generation of packaged foods. Its ability to reduce fat calories by up to 90%, while maintaining organoleptic performance across formats, gives it broad utility across both indulgent and health-conscious product lines.

Private-label manufacturers are expected to remain at the forefront of early adoption. These contract-based producers, often supplying leading retailers in North America and Europe, operate with tighter margins and stricter compliance thresholds, particularly in institutional procurement (such as school lunches, healthcare settings, and government programs). EPG allows these producers to reformulate quietly, maintain cost competitiveness, and meet new calorie or fat restrictions without triggering a decline in taste scores or consumer repurchase.

In the medium term, large multinational food companies may follow suit—but with more strategic integration models. Licensing deals, toll manufacturing agreements, or even equity stakes in Epogee-like ventures could allow global players to retain flexibility while locking in supply security. Analysts anticipate that tier-1 CPG brands will likely deploy EPG in pilot markets first—particularly in regions facing HFSS marketing bans, front-of-pack label mandates, or rising sugar/fat taxes. If consumer feedback and regulatory scorecards remain positive, these pilot launches could expand into core SKUs over a 24–36 month timeframe.

Moreover, EPG’s relevance is likely to grow as food companies seek portfolio-wide macronutrient harmonization—standardizing formulations across multiple brands to meet both internal ESG targets and external labeling regulations. Its GRAS status in the U.S., coupled with its non-disruptive formulation profile, allows for seamless integration into desserts, bakery, dairy, frozen, and snacking categories. As front-of-pack scoring systems such as Nutri-Score, HSR (Health Star Rating), and SmartLabel continue to influence consumer choice, EPG can serve as an enabler of category compliance without brand dilution.

From an investor and retailer standpoint, the scalability of EPG also supports stronger ESG narratives. It offers measurable impact in terms of caloric reduction per serving and supports reformulation targets aligned with WHO and CDC dietary guidelines. As institutional buyers—particularly retailers with in-house wellness brands—seek to meet their own carbon, calorie, or health portfolio goals, ingredients like EPG become value multipliers, not just cost line items.

Ultimately, EPG is poised to evolve beyond its role as a premium fat substitute. It could become the cornerstone of a commercially scalable calorie-reduction framework that balances taste, label compliance, consumer loyalty, and retailer demands. If supply can meet the demand and legal access remains equitable, EPG may define the next wave of silent, systemic health upgrades in packaged food—not by making food less indulgent, but by making indulgence smarter.

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.