Why Did Super Micro Cut Its Q3 FY2025 Outlook?

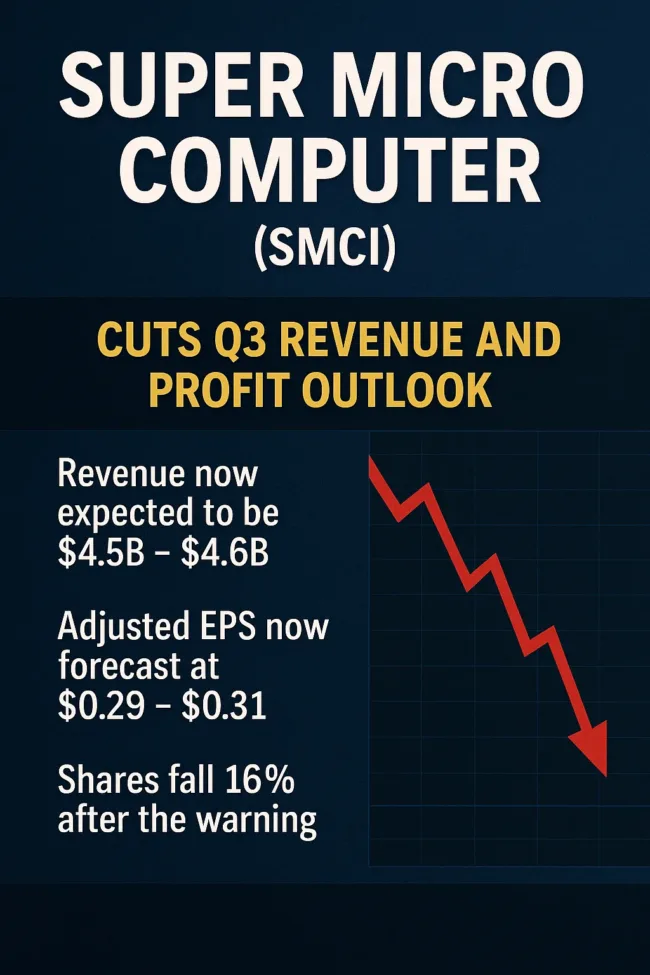

Super Micro Computer Inc. (NASDAQ: SMCI), a leading U.S.-based manufacturer of AI-optimized servers, has revised its fiscal third-quarter 2025 revenue and profit expectations downward, raising questions about the pace and predictability of AI infrastructure investments. On April 30, 2025, the company announced new guidance anticipating revenue between $4.5 billion and $4.6 billion, significantly below its prior estimate of $5.0 billion to $6.0 billion. Adjusted earnings per share (EPS) were also revised down to between $0.29 and $0.31, from the previously forecasted range of $0.46 to $0.62.

Super Micro attributed the downgrade to delayed customer platform decisions, which the company expects will shift revenue recognition into the fourth quarter. Management cited the timing of AI system deployments and platform transitions—particularly around Nvidia’s newly introduced Blackwell architecture—as key factors influencing purchasing behavior in the short term.

What Was the Market Reaction to Super Micro’s Warning?

The announcement prompted a sharp correction in Super Micro’s stock price, with shares falling approximately 16% in after-hours trading. The market selloff spilled into other technology names tied to AI infrastructure, including Nvidia Corporation, Dell Technologies Inc., and Hewlett Packard Enterprise Company, signaling broader anxiety about the timing of enterprise spending on generative AI and data center modernization.

While some investors interpreted the move as an isolated execution issue, others saw it as a potential early indicator of tightening IT budgets or changing procurement patterns amid global economic uncertainty. Analysts emphasized that such disruptions are not uncommon in high-growth sectors undergoing rapid technological transitions.

What’s Driving Delays in AI Infrastructure Spending?

Industry insiders suggest that the shift to next-generation GPU platforms—most notably Nvidia’s Blackwell series—has led many enterprise and cloud clients to delay orders, awaiting the full release of updated server configurations. Super Micro is a key partner for Nvidia and AMD, with server systems designed to support large-scale AI model training and inferencing. However, the fast-evolving nature of these workloads has introduced logistical complexities into customer planning cycles.

The delays also reflect broader shifts in AI deployment strategies. Many organizations are rebalancing their investments between core training infrastructure and edge/inference systems. The result is a more fragmented AI hardware landscape that complicates short-term demand forecasting for vendors like Super Micro.

What Are Investors and Institutions Doing With SMCI Stock?

Following the forecast revision, institutional sentiment around Super Micro Computer remains divided. According to the latest 13F filings, approximately 84.06% of SMCI shares are held by institutional investors, including Vanguard Group Inc., BlackRock Inc., and State Street Corp. The revised guidance has prompted mixed activity: some institutions are paring back exposure due to near-term visibility concerns, while others see the current pullback as an opportunity to accumulate shares in a company well-positioned for the next leg of AI infrastructure growth.

Bloomberg and Nasdaq flow data show modest net outflows from SMCI-focused ETFs in the immediate aftermath of the announcement. Short interest has increased slightly, suggesting hedge activity ahead of the company’s May 6 earnings call. Nonetheless, the overall level of institutional support remains structurally intact.

Equity research analysts remain cautiously optimistic. While most have placed their recommendations under review, several brokerage firms—including BofA Securities and Morgan Stanley—suggest holding the stock until the Q4 pipeline becomes clearer. Based on current valuation multiples and cash flow trends, SMCI is now broadly considered a “Hold” with upside potential if Q4 order deferrals are realized as projected.

Is the AI Server Market Slowing or Just Rebalancing?

The lowered forecast from Super Micro has raised valid concerns about AI server demand, but experts suggest that the industry is not experiencing a broad-based slowdown. Instead, the market is adjusting to a more nuanced deployment environment. Enterprises are no longer investing indiscriminately in large GPU clusters. Instead, purchasing is now guided by specific AI use-case ROI, regulatory readiness, and alignment with next-gen chip cycles.

Spending on AI infrastructure remains strong but is moving in phases. Enterprises are also increasingly factoring in power efficiency, thermal design, latency management, and liquid cooling technologies—all of which affect how quickly servers can be deployed and scaled. Super Micro’s modular, build-to-order design philosophy positions it well in this environment, but timing misalignments will continue to impact near-term financials.

What to Watch for in the Upcoming Q3 Earnings Call?

Super Micro has scheduled its Q3 FY2025 earnings call for May 6, during which it plans to provide detailed commentary on the deferred sales, revised customer timelines, and integration of Nvidia’s Blackwell GPUs into its server platforms. Investors will look for updates on regional demand dynamics, particularly in Asia and North America, where AI infrastructure buildouts are accelerating.

Analysts also expect the company to shed light on gross margin trends, supply chain stability, and capital expenditure plans. Any indication of improved visibility for Q4 and FY2026 could help stabilize the stock and renew institutional confidence.

Despite the near-term turbulence, Super Micro remains a core player in the global AI infrastructure stack. Its strong alignment with hyperscalers and semiconductor leaders such as Nvidia and AMD ensures that it will benefit from the continued expansion of AI data centers. However, the stock’s high valuation and sensitivity to execution risks make it prone to sharp corrections in response to guidance misses.

From a strategic perspective, the transition to liquid-cooled, high-density AI racks offers Super Micro a key differentiation opportunity. The company’s emphasis on short lead times, modular assembly, and flexible customization supports its competitiveness in a rapidly evolving market. If Q4 revenue ramps in line with management’s expectations, the current pullback may be viewed retrospectively as a consolidation phase before the next growth wave.

Super Micro’s lowered Q3 FY2025 guidance has jolted investor confidence and raised broader concerns about the pacing of AI infrastructure spending. While the company maintains that demand remains intact and merely delayed, the episode underscores the complexity of navigating capital-intensive, innovation-driven cycles in the AI server market. For investors, the key will lie in the next few quarters—particularly whether Super Micro can capitalize on deferred demand, manage platform transitions effectively, and reassure the market of sustained long-term momentum.

Share this:

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.