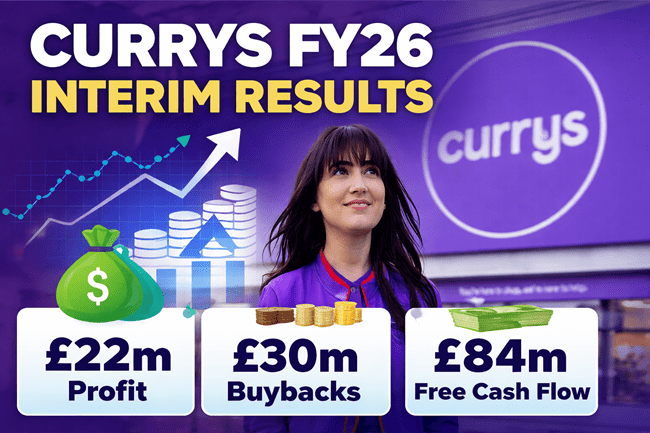

Currys plc (LSE: CURY) reported an adjusted profit before tax of £22 million for the half-year ended 1 November 2025, marking a sharp 144 percent year-on-year increase, driven by strong execution in the Nordics, growth in high-margin recurring services, and a disciplined capital return programme. Despite continued cost headwinds in the UK and Ireland, the company reaffirmed its full-year outlook, maintaining momentum in profit and free cash flow while completing 60 percent of its announced £50 million share buyback programme. Currys’ share price responded with an 8.14 percent intraday jump on 18 December 2025, closing at 136.90 GBX as investors digested the company’s positive operational and financial signals.

The performance highlights a strategic contrast across Currys’ regional segments. While the UK and Ireland showed resilience in revenue and service attachment rates, adjusted EBIT declined due to wage inflation and increased National Insurance costs. In contrast, the Nordics delivered a near doubling in profit, aided by strong online sales growth, margin stability, and deliberate avoidance of low-return sales. With net cash closing at £133 million and recurring service revenue rising across the group, the company signaled confidence through a reinstated dividend and continued execution of its share repurchase programme.

How is Currys plc driving profit growth despite UK retail cost pressures and uneven demand recovery?

Currys plc achieved an 8 percent increase in group revenue year-on-year, reaching £4,230 million for the first half of FY26, supported by a 4 percent like-for-like uplift and a balanced contribution from both its UK and Nordic operations. Adjusted EBIT rose to £54 million, up 32 percent over the prior period, while adjusted earnings per share improved from 0.6 pence to 1.6 pence. The company also posted an 11 percent increase in recurring service revenue in the UK, which now represents 13 percent of segment sales, with total high-value service revenue including credit accounting for 30.4 percent of UK revenue.

Within the UK and Ireland segment, revenue increased by 6 percent to £2,474 million, and Currys gained 60 basis points of market share in a declining consumer electronics and mobile market. However, adjusted EBIT declined by 17 percent to £19 million, driven by government-mandated cost increases. Gross margins declined by 40 basis points and were only partially offset by operational efficiencies and tight cost management. Additional investments in marketing and customer experience initiatives also added to the pressure on operating costs. The resulting EBIT margin dropped 20 basis points to 0.8 percent.

Despite the margin compression, the company expanded its credit adoption to 23.3 percent, up 160 basis points from the prior year. Currys now serves 2.8 million credit customers and reported £0.5 billion in credit-related sales during the period, representing a 12 percent year-on-year increase. New category growth also contributed to the top line, with health and beauty technology, gaming accessories, and AI-enabled computing seeing significant traction. Recurring revenue services and credit collectively offer stronger customer stickiness, longer lifetime value, and higher-margin contribution, reinforcing the company’s service-led strategy in a slower UK consumer environment.

What is powering the Nordics profit recovery and why is it outperforming the UK and Ireland business?

The Nordics region has emerged as the clear profit engine for Currys plc in this reporting cycle. Revenue grew by 11 percent year-on-year to £1,756 million, with a 7 percent increase on a currency-neutral basis. Adjusted EBIT nearly doubled, rising 94 percent to £35 million, while EBIT margin expanded to 2.0 percent, up 90 basis points compared to the same period last year. Operating cash flow increased by 59 percent to £43 million, and segmental free cash flow recovered sharply from a negative £4 million last year to £40 million this period.

The improvement in profitability came without sacrificing pricing discipline. Currys maintained stable gross margins in the Nordics and consciously avoided chasing low-margin sales, particularly in Finland. While this resulted in a 60 basis point decline in market share, it allowed the company to preserve margin integrity and generate significant operating leverage. Online revenue grew by 20 percent on a currency-neutral basis, contributing meaningfully to the region’s overall revenue mix and supporting efficiency gains.

The launch of Giga Mobiili, a mobile virtual network operator in Finland, also exceeded expectations in terms of subscription growth and market reception. The move is part of Currys’ strategy to replicate the success of iD Mobile in the UK, where the subscriber base reached 2.4 million, up 21 percent year-on-year. By offering bundled connectivity and services, the company is deepening its presence in customer ecosystems and driving higher retention rates across both consumer and small business segments.

The Nordics also saw rapid growth in new categories and emerging technology products. Robo vacuums and robotic mowers posted strong year-on-year gains, and computing hardware remained a standout performer. Store sales increased despite a reduction in store count, further validating Currys’ omnichannel strategy in this geography.

What does the capital return programme say about Currys plc’s financial discipline and shareholder positioning?

Currys plc entered the second half of FY26 with a net cash position of £133 million, up £26 million year-on-year, even after absorbing significant outflows. The company paid £82 million in pension contributions during the first half as part of its revised triennial agreement, reinstated its interim dividend at 0.75 pence per share, and completed £30 million of a planned £50 million share buyback programme.

The capital return policy signals a clear shift in how the company is managing surplus cash. In addition to maintaining a net cash balance above £100 million, Currys plans to continue paying down its pension liabilities, with scheduled contributions falling to £13 million annually from FY27 onward. The company has committed to growing the dividend progressively while using excess cash for buybacks, subject to maintaining balance sheet flexibility.

With adjusted EBITDAR margins rising to 4.6 percent and free cash flow jumping 68 percent to £84 million, the business appears to have regained its ability to deliver capital returns without compromising investment in core operations. Capex is projected to remain below £100 million annually, and exceptional cash costs are expected to fall below £10 million by FY27, aligning with Currys’ broader goal of improving cash conversion.

The buyback has likely contributed to the recent surge in the company’s stock price, which climbed more than 8 percent on 18 December. Investors appear to be rewarding the company’s mix of earnings visibility, cash discipline, and confidence in long-term structural drivers such as services, credit, and B2B expansion.

What execution risks could disrupt Currys plc’s recovery momentum in FY26 and beyond?

Despite the strong first-half showing, several execution risks could challenge Currys plc’s trajectory. The company made the strategic decision to delay its UK server migration to the cloud following operational issues encountered during the summer. Although this move prevented customer disruption during the critical Peak trading period, it will result in additional exceptional costs from dual systems running in parallel.

In the UK, ongoing wage inflation, National Insurance pressures, and business rate increases could further compress margins if not matched by efficiency gains or volume leverage. The success of new category expansion and B2B scaling depends heavily on execution at the store and fulfilment levels, as well as maintaining a seamless omnichannel customer experience.

In the Nordics, maintaining recent performance gains amid currency volatility and evolving consumer sentiment will require sustained investment in digital platforms and careful balancing of pricing and market share. Additionally, expanding services like mobile connectivity and repair operations introduces operational complexity, especially across fragmented regulatory environments and varying consumer behavior in the region.

There is also some credit risk exposure embedded in the growth of consumer financing. While Currys has highlighted high-quality underwriting and diversified credit portfolios, a sudden macroeconomic downturn could affect repayment rates or limit the expansion of retail credit.

Key takeaways on what Currys plc’s FY26 interim results reveal about strategy, profitability, and investor positioning

- Currys plc delivered a sharp earnings recovery in H1 FY26, with adjusted profit before tax up 144 percent year on year and adjusted EBIT rising 32 percent, confirming that recent operational changes are translating into measurable financial outcomes.

- The Nordics emerged as the group’s primary profit engine, with adjusted EBIT nearly doubling to £35 million and margins expanding by 90 basis points, driven by strong online growth, disciplined pricing, and a deliberate focus on profitability over market share.

- UK and Ireland performance remained resilient but margin constrained, as revenue grew 6 percent and market share increased, while adjusted EBIT fell 17 percent due to wage inflation and National Insurance cost pressures that continue to weigh on retail economics.

- Recurring services and consumer credit are becoming structurally more important, with UK credit adoption rising to 23.3 percent and high value service revenue now accounting for more than 30 percent of UK sales, supporting customer retention and long-term margin stability.

- Cash generation strengthened materially, with free cash flow rising 68 percent to £84 million, allowing Currys to fund an £82 million pension contribution while still increasing net cash to £133 million.

- Capital allocation discipline is improving investor confidence, evidenced by the completion of £30 million of a £50 million share buyback programme and the reinstatement of an interim dividend, bringing total shareholder returns this year to £75 million.

- Short-term execution risks remain manageable but visible, particularly around UK cost inflation, deferred cloud migration expenses, and the expanding use of retail credit in a potentially volatile consumer environment.

- Strategically, Currys is repositioning itself as a service-led omnichannel platform, reducing reliance on low-margin hardware sales and increasing the likelihood of sustained cash flow, improved valuation support, and potential long-term interest from strategic or financial buyers.

Share this:

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.