Why is Banca Monte dei Paschi di Siena stock rallying after the Mediobanca offer results?

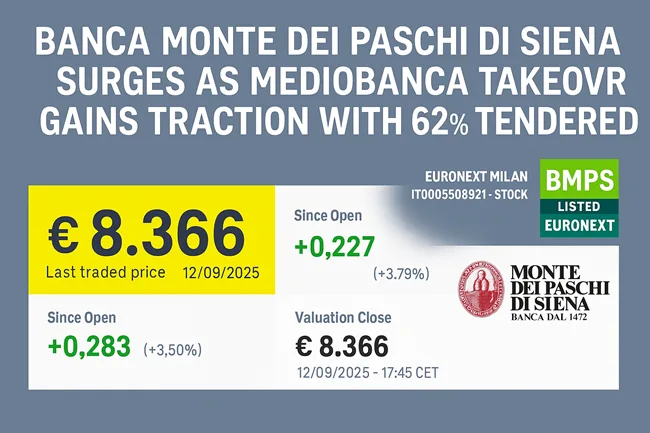

Banca Monte dei Paschi di Siena S.p.A. (Euronext Milan: BMPS) ended the September 12, 2025 trading session on a strong note, closing at €8.366. The share price was up 2.79 percent from the open and 3.50 percent compared to the previous close, signaling a clear bullish response from the market. The optimism was driven by confirmation of the final results of the bank’s voluntary public tender and exchange offer for Mediobanca – Banca di Credito Finanziario S.p.A., one of Italy’s most prominent investment banks.

The Siena-based institution announced that 62.3 percent of Mediobanca’s share capital had been tendered, effectively securing majority control and reinforcing its ambition to lead Italy’s next wave of banking consolidation. The final tally matched earlier provisional results released in the first week of September, removing uncertainty and setting the stage for completion. Payment of the overall consideration, a mix of newly issued BMPS shares and a cash component of €0.90 per Mediobanca share, is scheduled for September 15, 2025.

This outcome has been interpreted by investors as an inflection point for BMPS. The bank, long associated with bailouts and restructuring challenges, is positioning itself not as a relic of past financial crises but as an active consolidator capable of reshaping Italy’s financial sector.

What does the Mediobanca takeover mean for BMPS’s business model and balance sheet?

Banca Monte dei Paschi di Siena is the world’s oldest bank still in operation, founded in 1472, and a fixture in Italy’s banking history. For decades it served as a regional powerhouse in Tuscany before expanding nationwide. The global financial crisis, combined with Italy’s sovereign debt turmoil and risk management missteps, forced the bank into state-backed rescues and years of painful restructuring. Today’s takeover of Mediobanca signals that the bank is once again playing offense rather than defense.

The Mediobanca acquisition brings diversification across segments that align with BMPS’s four core activities. In commercial banking, BMPS already serves retail and corporate clients through more than 1,300 branches in Italy, offering everything from standard current accounts to leasing, factoring, and consumer loans. The addition of Mediobanca deepens BMPS’s presence in corporate finance and high-end private banking, broadening its revenue sources beyond traditional lending.

On the investment banking side, BMPS gains exposure to Mediobanca’s structured financing capabilities, advisory services, and venture capital initiatives, particularly in industries such as food processing and environmental engineering. This complements BMPS’s existing corporate finance practice and provides a platform to compete more effectively with larger peers like UniCredit and Intesa Sanpaolo.

In asset management, BMPS will benefit from Mediobanca’s established wealth management franchises and distribution networks. Meanwhile, in bank-insurance services, the merger adds depth to a segment where Mediobanca historically leveraged ties with Generali and other insurers. Together, the combination enhances BMPS’s ability to cross-sell and capture more value across its client base.

Financially, the merger is transformative. At the end of 2024, BMPS managed €82.6 billion in deposits and €87.2 billion in loans. By issuing 1.28 billion new shares to Mediobanca shareholders, BMPS will more than double its capital base to 2.54 billion ordinary shares. While this dilutes existing shareholders, it also creates a bank with greater scale, more diversified income streams, and a stronger competitive position in Italy’s crowded market.

How have investors and institutions reacted to the Mediobanca exchange offer?

Market sentiment has been broadly supportive, reflected in BMPS’s share price appreciation. The acceptance of over 62 percent of Mediobanca’s shares suggests significant alignment between the two shareholder bases and indicates that Italian funds, retail investors, and some foreign institutions saw value in BMPS’s proposition.

Trading on September 12 showed best bids around €8.23 and asks at €8.40, with heightened activity suggesting speculative flows alongside institutional positioning. Analysts believe that the September 2 decision to add a cash sweetener of €0.90 per Mediobanca share played a pivotal role in convincing shareholders to tender their stakes.

Foreign institutional investors remain cautious, with some voicing concerns about integration costs, cultural differences between the banks, and the impact of state ownership on governance. However, the prevailing narrative is that consolidation is necessary, and BMPS’s bold move could create shareholder value if execution is handled well. The market is interpreting this as a “buy on consolidation” opportunity, which explains the supportive sentiment.

What comes next after the Mediobanca acceptance and BMPS’s payment date?

With final results confirmed, BMPS is preparing to settle the transaction. On September 15, 2025, shareholders who tendered their Mediobanca stakes will receive 2.533 newly issued BMPS shares and €0.90 per share in cash. For investors who held back, a reopened acceptance window will run from September 16 to September 22, offering one final chance to participate on the same terms.

This secondary window could lift BMPS’s control beyond 62.3 percent, potentially strengthening its ability to implement governance changes and accelerate integration. Payment for shares tendered during the reopened period will take place on September 29, ensuring a rapid conclusion to the transaction.

Post-deal, the focus shifts to integration. Analysts expect challenges in rationalizing branch networks, aligning corporate cultures, and retaining top talent in both organizations. Yet they also highlight opportunities for cost synergies, especially in overlapping retail operations, and for revenue growth through combined corporate finance and wealth management businesses.

How does this fit into Italy’s broader banking consolidation wave?

BMPS’s acquisition of Mediobanca represents the largest Italian banking merger in years and reflects ongoing pressure from European regulators to streamline the sector. Italy has long had a fragmented banking landscape, with many mid-sized lenders struggling to compete with larger European rivals. The European Central Bank has consistently encouraged consolidation as a way to reduce systemic risk and create stronger, more resilient institutions.

For BMPS, this move positions it alongside Italy’s heavyweights. Intesa Sanpaolo has dominated the domestic market following its acquisition of UBI Banca in 2020, while UniCredit remains a cross-border European giant. By absorbing Mediobanca, BMPS enhances its profile in investment banking and wealth management, areas where it previously lagged.

The transaction recalls earlier consolidation milestones such as UniCredit’s acquisition of HypoVereinsbank in Germany and Intesa’s merger with Sanpaolo IMI. However, BMPS’s case is unique, given its crisis-ridden past and ongoing state involvement. Success here could redefine the narrative around BMPS from bailout survivor to consolidation leader.

Can the optimism around Banca Monte dei Paschi di Siena stock last, or will institutional flows and integration risks cap the rally?

Investor enthusiasm around BMPS’s stock reflects both confidence and speculation. Domestic institutional investors appear to be leaning toward accumulation, encouraged by the opportunity to back a newly empowered Italian banking champion. Foreign institutional investors are adopting a wait-and-see approach, balancing the upside of consolidation against execution risks.

Flows in recent sessions suggest that retail investors have played an outsized role in pushing up BMPS’s stock price. The €8.20 to €8.40 range has become an important technical band, with traders watching whether the stock can break decisively above €8.50. Such a move on heavy volume could trigger additional institutional interest.

Short-term volatility is inevitable as BMPS’s enlarged share capital begins trading. Long-term funds are expected to hold through the dilution, betting that the combined entity will generate stronger fee income and synergies that outweigh integration costs. The durability of optimism will depend on management’s ability to execute integration smoothly and maintain credit quality in a challenging macroeconomic environment.

What is the outlook for BMPS stock and investor positioning?

Looking forward, the market will judge BMPS on its ability to deliver results, not simply announce bold plans. Investors will be watching closely for evidence that cost savings are being realized from overlapping branch networks, that Mediobanca’s investment banking franchise is being effectively integrated, and that wealth management synergies are materializing.

Analysts also expect further consolidation in the Italian banking sector. BMPS, now armed with Mediobanca’s scale and capabilities, could play a leading role in shaping future mergers. If successful, this transaction could transform BMPS from a bank weighed down by crisis history into a central pillar of Italy’s financial system.

The outlook is cautiously optimistic. Execution risks remain, but BMPS is no longer viewed as a passive survivor of past bailouts. Instead, it has taken the initiative to reshape Italy’s banking landscape. For investors, the coming months will provide critical signals on whether this is the beginning of a sustained re-rating or a temporary bounce.

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.