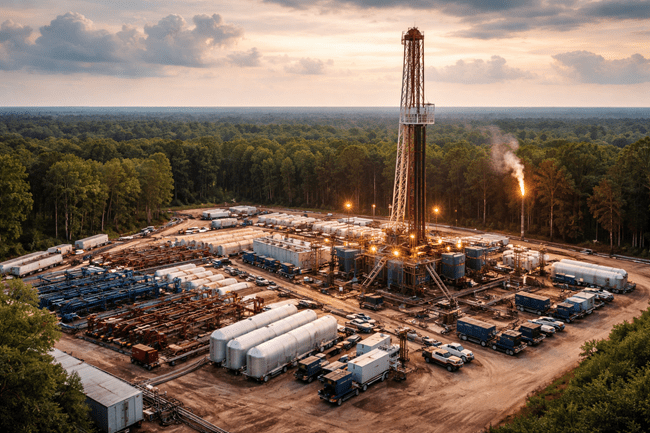

Mitsubishi Corporation has signed a definitive agreement to acquire 100 percent equity in Aethon III LLC, Aethon United LP, and associated entities operating across the Haynesville Shale formation in Texas and Louisiana. The all-cash deal, announced on January 16, 2026, is valued at approximately $5.2 billion and marks the company’s first direct entry into U.S. shale gas production. The transaction, which also includes assumption of $2.33 billion in net debt, is expected to close in the first quarter of Japan’s fiscal year 2026, subject to regulatory approvals.

The acquisition not only gives Mitsubishi Corporation full upstream access to one of North America’s most productive gas basins but also positions the company to build an end-to-end LNG value chain spanning exploration, liquefaction, marketing, and export. With production already at 2.1 billion cubic feet per day and capacity expected to rise to 2.6 billion cubic feet per day, the assets represent a strategic foothold in a region increasingly central to both domestic energy flows and LNG export corridors.

Why Mitsubishi Corporation is doubling down on U.S. gas in the age of LNG demand divergence

The timing of Mitsubishi Corporation’s move reflects both structural energy market realignments and the company’s deliberate pivot from passive offtake to active upstream control. For over a decade, the company has played a downstream role in global LNG markets through equity stakes in liquefaction projects like LNG Canada and Cameron LNG. This acquisition flips the model. By owning the gas at the source, Mitsubishi Corporation can extract more value across the chain while insulating itself from input volatility and contract exposure.

Aethon’s Haynesville acreage provides precisely the kind of high-productivity, cost-efficient gas that large-scale LNG operations demand. Located in proximity to Gulf Coast terminals such as Cameron LNG, the asset suite reduces both transport costs and congestion risk. This locational advantage also supports optimized sales portfolios that mix domestic sales into the U.S. South with international cargoes shipped to Asia and Europe.

More importantly, Haynesville’s strong correlation with the Henry Hub benchmark allows Mitsubishi Corporation to align pricing and hedging strategies across global portfolios, offering flexibility in managing commodity risk and regional spreads.

Connecting the dots: How Aethon complements Mitsubishi Corporation’s energy and power platform

This deal is not just about acquiring barrels of gas. It plugs directly into Mitsubishi Corporation’s expanding North American energy platform, which already includes Canadian shale gas projects with Ovintiv, gas marketing via Houston-based CIMA Energy, and downstream infrastructure through Diamond Gas International and Diamond Generating Corporation. Taken together, these assets form a cross-border gas-to-power ecosystem.

Mitsubishi Corporation intends to create new synergies between Aethon’s production capacity and its own LNG marketing and electricity businesses. Aethon’s in-house midstream infrastructure, including gas processing facilities and trunk pipelines, enables sales optimization without relying on third-party tolling or transport providers. This is particularly critical as the company eyes integration into clean hydrogen and gas-to-chemicals production.

The acquisition also aligns with Mitsubishi Corporation’s strategy to deepen vertical integration in North America, where LNG export growth, AI-driven data center power demand, and regional reindustrialization are reshaping natural gas fundamentals. By anchoring upstream operations in the U.S. South, the company is positioning itself to meet this multi-dimensional demand with reliable, low-cost feedstock.

What this acquisition reveals about capital allocation under Corporate Strategy 2027

From a financial standpoint, the acquisition is framed under Mitsubishi Corporation’s “Corporate Strategy 2027,” specifically the value creation pillar called “Create.” The company expects the Aethon assets to generate ¥270 billion to ¥300 billion in underlying operating cash flow and ¥70 billion to ¥80 billion in net income annually by fiscal year 2027. These figures represent a meaningful uplift to overall group profitability and position the deal as a cornerstone of the company’s near-term capital returns strategy.

To maintain its targeted net debt-to-equity ratio of approximately 0.6, Mitsubishi Corporation is deploying a mix of equity, divestiture proceeds, and strategic leverage. Management has made clear that the capital structure can absorb the additional debt from the Aethon deal without impairing liquidity or share buyback capacity.

Mitsubishi Corporation also plans to maintain financial flexibility through optionality embedded in the transaction. Aethon Energy Management retains the right to repurchase up to 25 percent of the upstream and midstream assets. This mechanism could allow the company to recycle capital depending on commodity cycles or co-investor interest, while still preserving operational control and integration benefits.

From decarbonization to diversification: The multipolar logic behind Mitsubishi Corporation’s shale gas play

The deal sits at the intersection of three overlapping drivers: energy security, decarbonization, and revenue diversification. First, the acquisition gives Mitsubishi Corporation direct access to stable gas volumes in a market where geopolitical and weather-related shocks have heightened the importance of secure supply. Second, the company has emphasized that the assets comply with rigorous environmental standards. Aethon has cut methane and carbon dioxide emissions intensity by 40 to 50 percent over the past five years, reflecting alignment with global ESG expectations.

Third, this transaction enables Mitsubishi Corporation to pursue multi-product monetization. Beyond LNG, gas from Aethon could feed electricity generation for hyperscale data centers, power chemical production, or serve as a transition fuel for clean hydrogen hubs. With the Energy and Power Solutions Group set to launch in April 2026, the company is preparing to coordinate these gas-derived businesses through a single command center, enhancing coherence across its North American footprint.

This approach mirrors the company’s evolving investment philosophy: allocate capital to infrastructure-adjacent platforms that offer long-term upside and downside protection. Previous divestitures in fast-food, apparel retail, and underperforming joint ventures were designed to free up balance sheet capacity for just this kind of industrial-scale pivot.

Why this matters for global LNG markets and competitors in the shale ecosystem

For the global LNG market, Mitsubishi Corporation’s move sends a strong signal. Japanese trading houses, traditionally more passive in LNG operations, are now seeking upstream control as a hedge against both price swings and geopolitical friction. It also reflects rising institutional consensus that LNG will remain a foundational energy vector, not merely a transitional fuel.

For North American peers like ConocoPhillips, EQT Corporation, and Chesapeake Energy, Mitsubishi Corporation’s entrance adds a new class of competitor—one that brings not just capital, but also downstream offtake, cross-border trading leverage, and sovereign-aligned energy objectives.

It also raises the bar for how upstream gas producers think about integration. In an increasingly interconnected energy economy, ownership of physical molecules is no longer sufficient. The ability to flow those molecules through global routes, backed by long-term buyer relationships and flexible hedging strategies, is where the margin and resilience now lie.

What institutional investors should track as Mitsubishi Corporation executes on this platform build

Execution risk remains. Integrating a private-equity-backed shale gas operation into a publicly listed conglomerate with layered governance and ESG scrutiny will require operational discipline and cultural alignment. Additionally, the timing and structure of any potential 25 percent re-entry by Aethon Energy Management must be monitored for valuation resets or operational divergence.

That said, Mitsubishi Corporation’s existing presence in Canadian upstream and U.S. marketing reduces the risk of being a naïve entrant. The company has also demonstrated balance sheet rigor in past resource investments, and its current debt and cash flow positions provide room for temporary shocks.

Institutional investors tracking this move should focus on three markers over the next 12 to 18 months. First, how successfully Mitsubishi Corporation ramps production from 2.1 billion cubic feet per day to 2.6 billion. Second, the degree of margin uplift achieved through LNG export versus domestic sales. And third, how the Aethon assets are operationally linked to other business segments such as data center power supply, hydrogen, and chemical manufacturing.

This is not simply a production acquisition. It is a signal of long-term intent.

Key takeaways on what this development means for Mitsubishi Corporation, its competitors, and the industry

- Mitsubishi Corporation has made a decisive $5.2 billion acquisition of Aethon’s Haynesville Shale gas business, gaining direct upstream access in the U.S. South.

- The acquisition delivers 2.1 billion cubic feet per day of production with upside to 2.6 billion, positioning Mitsubishi Corporation as a significant shale gas operator.

- By integrating Aethon with its existing infrastructure, the company is building a full-cycle LNG value chain across North America.

- This aligns with Corporate Strategy 2027 and is expected to generate up to ¥300 billion in operating cash flow and ¥80 billion in net income by FY2027.

- Optionality in the deal structure, including a 25 percent re-entry right for Aethon Energy Management, provides future capital management flexibility.

- Mitsubishi Corporation is positioning the asset to serve not just LNG, but also power generation, hydrogen, and chemical manufacturing in the Gulf Coast industrial corridor.

- Sustainability measures already in place at Aethon reduce ESG integration risk, and emissions intensity has already declined by nearly half.

- With LNG demand rising in both Asia and Europe, Mitsubishi Corporation gains the ability to arbitrage domestic and export gas flows under one operational umbrella.

- The move also signals rising verticalization among Japanese trading houses, which are evolving from buyers to full-cycle energy platform builders.

- For institutional investors and global LNG competitors, this marks a shift in how upstream gas will be priced, marketed, and monetized in the next phase of energy transition.

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.