MS International plc (LON: MSI) has secured new defence contracts with the United States Navy worth a combined $42.1 million, underscoring both the company’s operational momentum and its deepening strategic role within global naval systems supply chains. The development marks one of the largest U.S. awards yet for the British defence manufacturer, coming through its wholly owned American subsidiary, MSI-Defence Systems US LLC, based in Rock Hill, South Carolina.

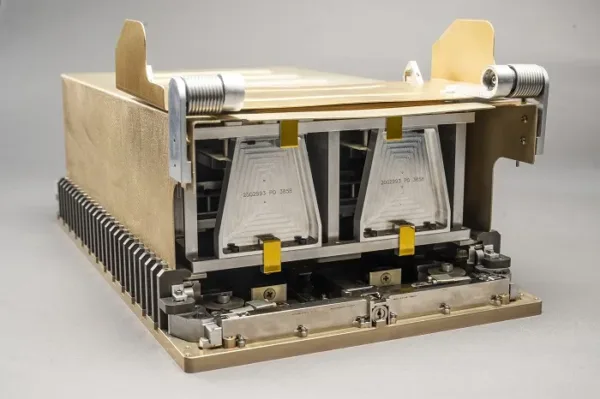

The primary contract, valued at $34.5 million, was awarded by the U.S. Naval Sea Systems Command (NAVSEA) on a sole-source basis — a move that reinforces the Navy’s reliance on MS International’s proven systems and sustained performance record. The order covers the continued supply of the MK88 MOD4 MSI-DS stabilised gun mounts, along with maintenance assist modules and onboard repair parts. Deliveries are scheduled to be completed no later than 30 December 2026.

The deal follows MS International’s successful response to a Request for Quotation (RFQ) referenced in Chairman Michael Bell’s statement during the company’s 2025 Annual Report. Importantly, the contract’s sole-source nature demonstrates the degree of technical integration and trust built between MSI and the U.S. Navy, reflecting years of collaboration in shipboard weapons and sighting systems.

In addition to the primary order, the company also confirmed a contract amendment worth $7.6 million for its ongoing supply of electro-optical sight systems, known under U.S. Navy nomenclature as the Mk48 MOD2 Electro-Optical Sight System. These advanced sensor and targeting systems are part of MSI’s integrated 30 mm weapon platforms. Deliveries for this amendment are expected by 30 November 2026, further bolstering the company’s U.S. production pipeline.

Why is this contract strategically important for MS International’s long-term defence positioning?

The contracts mark more than just incremental revenue growth — they solidify MS International’s presence as a trusted supplier to one of the world’s largest defence clients. The continued partnership with NAVSEA showcases the company’s capacity to meet stringent U.S. procurement standards while aligning with evolving naval combat requirements such as stabilised, remote-controlled weapon systems.

Although earlier shareholder communications had hinted at hopes for a longer-term framework contract, NAVSEA opted to move toward annual contracting cycles. For the U.S. Navy, this approach increases operational flexibility and allows more responsive procurement planning amid shifting global defence priorities. For MS International, it means recurring validation of performance — each annual renewal becoming an opportunity to demonstrate reliability, maintain system compatibility, and expand its footprint within the Navy’s modernisation programs.

Strategically, the company’s growing U.S. footprint also positions it advantageously amid increased transatlantic cooperation in defence manufacturing. With NATO partners scaling up industrial capacity, suppliers with established U.S.–U.K. dual presences are expected to benefit most. MSI’s South Carolina operations could play a pivotal role in fulfilling near-term and mid-term naval requirements while ensuring alignment with “Buy American” compliance frameworks.

How have the markets and investors reacted to MS International’s expanding defence portfolio?

Investors responded positively to the announcement, with MS International shares (LON: MSI) closing at 1,460 pence, up 1.04 percent on the day of disclosure. The stock, part of the FTSE AIM 100 Index, has displayed steady upward momentum through 2025 — appreciating roughly 40 to 46 percent over the past twelve months. Trading volumes remain moderate but healthy, suggesting ongoing accumulation by institutional investors following the company’s operational updates and order wins.

At these levels, the share price implies a price-to-earnings ratio of approximately 16 to 17 times, aligning with other mid-cap defence and industrial technology peers on the London market. The group’s latest annual report indicated revenue growth to £117.5 million, up from £109.6 million a year earlier, and a net profit of around £14.5 million, underscoring healthy operational leverage despite macro-economic headwinds. The dividend yield, hovering near 1.6 percent, provides additional reassurance to long-term investors seeking both growth and stability.

Market watchers observed that the latest U.S. Navy contracts provided a psychological boost to sentiment around MS International, signalling sustained demand visibility through 2026. The sole-source nature of the award was widely interpreted as evidence of the company’s proprietary know-how in maritime fire-control systems — a segment where few competitors offer comparable proven reliability.

What is the institutional and analyst sentiment surrounding MS International’s latest performance?

Institutional sentiment toward MS International remains broadly optimistic but tempered by the inherent cyclicality of defence contracting. Analysts tracking the AIM 100 defence cohort have highlighted MSI’s ability to translate niche engineering capabilities into long-term revenue streams. The consistency of U.S. Navy awards is viewed as a validation of the company’s systems reliability and export competitiveness.

Some analysts have described the new contract as a “confidence marker” rather than a one-off revenue spike, pointing to recurring opportunities if MSI maintains delivery timelines and quality benchmarks. Institutional investors appear to agree; the stock’s gradual re-rating over the past year has reflected increasing recognition of MSI as a specialist defence supplier rather than a small-cap outlier.

At the same time, observers note that the shift to one-year contracting frameworks introduces some visibility risk. Should budget adjustments or procurement reprioritisations occur within NAVSEA, renewals could slow. Nonetheless, given the enduring demand for shipboard defence modernisation across the U.S. fleet, most view this as a manageable operational variable rather than a structural threat.

What key operational and financial risks could challenge MS International’s ability to sustain contract-driven growth through 2026?

Despite strong fundamentals, MS International must navigate a few operational challenges. The most immediate is contract renewal risk tied to NAVSEA’s decision to award contracts annually. This approach demands continual performance excellence — timely deliveries, cost discipline, and minimal quality deviations. Any lapses could jeopardise subsequent awards.

Another consideration is exposure to supply-chain volatility, particularly in high-precision components used in electro-optical systems. While MSI’s dual-country footprint mitigates logistics risk, global shortages of specialised materials or electronic subsystems could create cost inflation.

Moreover, macro-economic factors such as currency fluctuations and geopolitical shifts could influence both input pricing and government procurement patterns. Analysts note that while defence budgets in NATO countries remain robust, political transitions or fiscal tightening cycles could affect future order flow. Still, MSI’s niche specialisation provides insulation from broader discretionary-spending cuts.

How could MS International’s defence business evolve over the next 24 months?

Looking forward, the newly announced contracts set the stage for a period of sustained growth and operational visibility for MS International. If execution remains strong, the company’s track record with NAVSEA could open doors to larger-scale, multi-year programs once procurement conditions stabilise.

The ongoing global re-armament trend, driven by geopolitical uncertainty and the need for advanced maritime deterrence systems, provides fertile ground for continued expansion. Analysts anticipate that MSI could diversify into adjacent naval-integration projects or extend its electro-optical expertise into surveillance and unmanned-system platforms — segments that align with its current technical portfolio.

From a capital-markets perspective, the company’s steady earnings trajectory and proven dividend discipline make it attractive to both growth-oriented and income-seeking investors. Institutional inflows could strengthen as MSI’s market capitalisation rises further within the AIM 100 universe, potentially attracting coverage from larger brokerage houses.

If NAVSEA’s annual renewals continue beyond 2026, each successive contract cycle would reinforce MSI’s credibility and contribute to compounding order-book visibility. The cumulative impact of consistent U.S. defence orders, growing international exposure, and stable financials may gradually reposition MS International from a niche manufacturer to a mid-tier defence player with global reach.

How do defence experts and market observers view MS International’s dual success across U.S. Navy contracts and investor confidence?

Industry observers interpret these U.S. Navy contracts as an early signal that MS International’s methodical, engineering-driven business model is finding new resonance in the era of defence industrial revitalisation. The dual structure of short-term contract renewals coupled with strong customer rapport offers a rare blend of agility and dependability.

For investors, the message is equally clear. The combination of expanding revenue, improving margins, and recurring defence demand provides a solid case for continued interest in MS International shares. As the company executes on these contracts through 2026, the next major catalysts could include follow-on orders, diversification into allied programmes, and the scaling of its U.S. subsidiary’s production capacity.

With the shares trading near multi-year highs and the underlying defence order book strengthening, the market seems to be recognising MS International as one of the AIM market’s more credible industrial success stories of 2025. The intersection of defence reliability and financial resilience positions it well for both operational and shareholder returns in the medium term.

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.