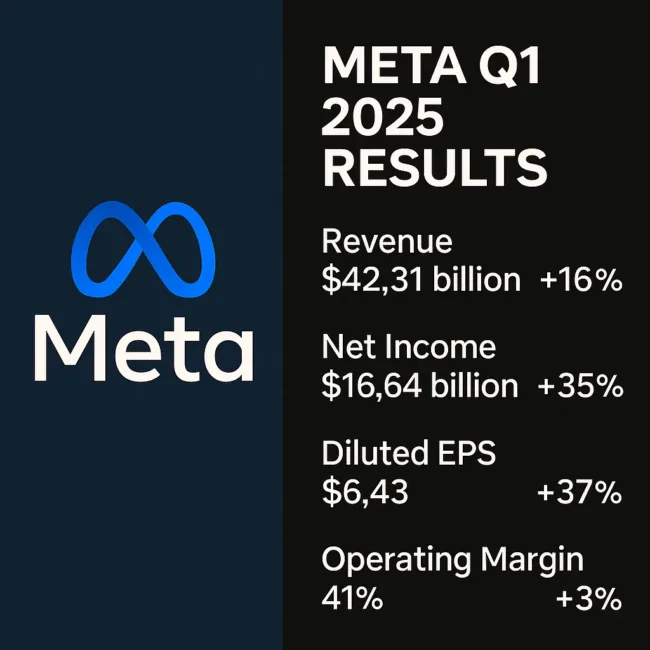

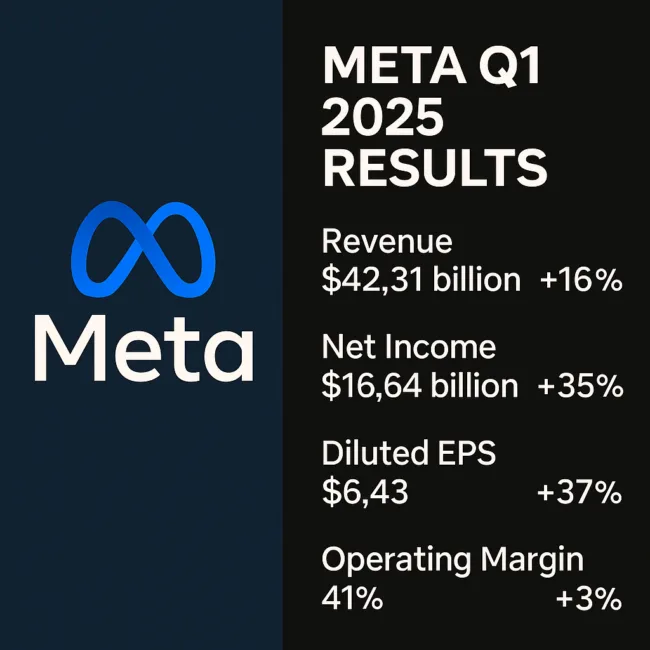

Meta Platforms Inc. (NASDAQ: META) posted a 35% year-over-year jump in net income to $16.64 billion for the first quarter of 2025, capping off a quarter marked by strong ad sales, increasing user engagement, and rapid expansion of its artificial intelligence offerings. Revenue rose to $42.31 billion, a 16% increase from Q1 2024, as the company leaned into scalable AI deployment and monetization across its platforms.

Founder and CEO Mark Zuckerberg described Q1 2025 as a “strong start to an important year,” citing Meta AI’s monthly user base of nearly one billion as a sign of the company’s progress toward making AI foundational across its product suite.

Meta’s Q1 performance reflects not only its dominance in digital advertising, but also the growing contribution of AI infrastructure investments and the potential long-term monetization of immersive technologies. However, that trajectory faces serious challenges from regulatory scrutiny, particularly in the European Union, which could reshape revenue and product deployment across Meta’s global markets.

How Strong Was Meta’s Core Financial Performance?

Meta reported operating income of $17.56 billion for the March-ended quarter, up 27% from the prior year, with operating margins expanding to 41% from 38%. Diluted earnings per share climbed to $6.43, a 37% year-on-year increase, comfortably beating analyst estimates. The company’s cost discipline—particularly in sales and general administrative categories—supported margin growth even as R&D spending surged.

Total expenses rose 9% year-over-year to $24.76 billion, driven mainly by research and development investments, which rose 22% to $12.15 billion. This reflects Meta’s aggressive expansion of its AI compute capabilities and longer-term metaverse ambitions.

Advertising continues to underpin Meta’s business model, with ad revenue of $41.39 billion accounting for over 97% of total revenue. On a constant currency basis, total revenue growth would have reached 19%. The average price per ad grew 10% year-on-year, and ad impressions rose 5%, pointing to strong pricing power and effective monetization.

What Drove Growth Across Meta’s Platforms?

Meta’s daily active user base across its Family of Apps—which includes Facebook, Instagram, Messenger, and WhatsApp—reached 3.43 billion in March 2025, up 6% year-over-year. The ability to maintain engagement growth at this scale indicates Meta’s effectiveness in personalization, recommendation engines, and cross-platform utility.

A significant part of this user engagement is being driven by the integration of AI into core experiences. Meta AI now powers search, feed ranking, messaging, and content discovery, contributing both to user retention and monetizable engagement.

Meta is also actively exploring generative content creation features, including AI-generated Reels, conversational commerce agents, and new creator tools. These AI layers enhance stickiness while opening new avenues for revenue.

How Is Meta Deploying AI to Sustain Long-Term Growth?

Meta’s AI strategy spans foundational model training, deployment at scale, and user-facing tools. The company has committed to building some of the world’s largest AI training clusters, with custom silicon and optimized data centers. These are essential not only for inference workloads in ad delivery and content ranking, but also for broader ambitions in consumer-grade AI.

Capital expenditures for Q1 totaled $13.69 billion, reflecting large-scale investments in compute, storage, and networking infrastructure. Most of the spend was directed toward Meta’s core business rather than Reality Labs, underscoring that AI—not the metaverse—is currently at the center of operational focus.

This infrastructure push supports Meta AI, which has now reached significant product-market fit and usage. It also enables the company to compete with OpenAI, Google DeepMind, and Anthropic in the enterprise and consumer LLM markets.

What’s the Strategic Outlook for Reality Labs?

While Reality Labs continued to post operating losses—$4.21 billion in Q1 versus $3.85 billion last year—the division remains central to Meta’s long-term vision of immersive computing. Revenue from Reality Labs fell slightly to $412 million, pointing to continued soft demand for VR headsets and AR glasses.

However, Meta executives have reiterated that Reality Labs is a “multi-year investment in the future of computing.” Meta’s work on AR smart glasses, haptic feedback systems, and mixed-reality operating systems is viewed internally as analogous to building a smartphone platform in the mid-2000s.

While Wall Street remains divided on the financial timeline for Reality Labs payback, Meta’s willingness to fund this division without immediate ROI is viewed as a sign of strategic depth. The question for investors is whether immersive tech will eventually justify the capital outlay or remain a costly experiment.

How Are Regulatory Risks in Europe Shaping Meta’s Roadmap?

The European Commission recently ruled that Meta’s “subscription for no ads” model violates the Digital Markets Act (DMA), a sweeping EU regulation targeting gatekeeper platforms. According to Meta, the EC’s feedback suggests the company must make significant changes to this model, which could worsen the user experience for European audiences and lead to a meaningful hit to ad revenue starting in Q3 2025.

Meta intends to appeal the decision, but it has acknowledged that changes may be imposed before the appeal concludes. This adds urgency to compliance efforts and raises broader questions about Meta’s advertising model under DMA scrutiny.

Executives also flagged that similar regulatory pressures are building in the U.S., where data privacy legislation, platform accountability laws, and antitrust inquiries are intensifying. These developments could result in increased compliance costs, restricted personalization, and evolving ad targeting practices across jurisdictions.

How Is Meta Positioned Financially?

Meta ended the quarter with $70.23 billion in cash, cash equivalents, and marketable securities. Operating cash flow totaled $24.03 billion, while free cash flow stood at $10.33 billion after accounting for capital and lease-related outflows. The company returned $13.4 billion to shareholders via stock buybacks and paid $1.33 billion in dividends and equivalents.

Despite significant capital investment, Meta’s financial flexibility remains high. Strong cash generation allows the company to pursue simultaneous investments in AI, immersive tech, and shareholder returns—without leveraging its balance sheet excessively.

What Guidance Has Meta Issued for 2025?

For Q2 2025, Meta projects revenue between $42.5 billion and $45.5 billion, with a 1% benefit from currency tailwinds. Full-year expense guidance was lowered to $113–118 billion, from $114–119 billion previously, indicating efficiency improvements and greater cost discipline.

On the other hand, capital expenditure guidance was raised to $64–72 billion, up from $60–65 billion, as Meta ramps up its infrastructure buildout. Management reaffirmed its expected effective tax rate for 2025 at 12–15%, absent major changes in tax legislation.

What Do Markets and Institutions Think?

Meta’s Q1 results were well received by the market. Shares of Meta Platforms Inc. (NASDAQ: META) are currently trading at approximately $549.00, with a market cap of $1.45 trillion and a price-to-earnings ratio of 26.07. The stock posted an intraday high of $582.89 and a low of $529.82 following earnings, reflecting positive yet cautious investor reaction.

Institutional Flows and Analyst Ratings

Institutional participation remains strong. In Q1 2025, 2,283 institutional investors increased holdings in Meta, while 1,676 reduced exposure. Notably, Assenagon Asset Management S.A. added 2.2 million shares, signaling conviction in Meta’s AI and ad growth story.

Foreign Institutional Investors (FIIs) remained net buyers in Indian equities through April 2025, with ₹2,735 crore in net inflows, while Domestic Institutional Investors (DIIs) added ₹28,228 crore—suggesting favorable risk appetite across tech stocks globally.

Analyst sentiment is uniformly bullish. All 23 tracked research houses maintain a “Buy” or “Overweight” stance on META. Price targets range between $500 and $550+, driven by expectations of AI-led revenue growth, resilient monetization, and strategic capital deployment.

Investment Outlook: Buy, Hold, or Sell?

Meta remains a compelling long-term investment for institutional and retail investors focused on digital platforms, AI scalability, and capital efficiency. The stock continues to offer high returns on equity, strong free cash flow, and dominance in a growing ad market.

However, regulatory risks in Europe and ongoing scrutiny in the U.S. present non-trivial downside scenarios. While buy ratings dominate, prudent investors are watching for any deterioration in European ad revenue or user engagement due to legal changes.

At current levels, Meta remains a “Buy” with upside potential tied to its ability to operationalize AI across user touchpoints while navigating compliance across markets.

Share this:

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.