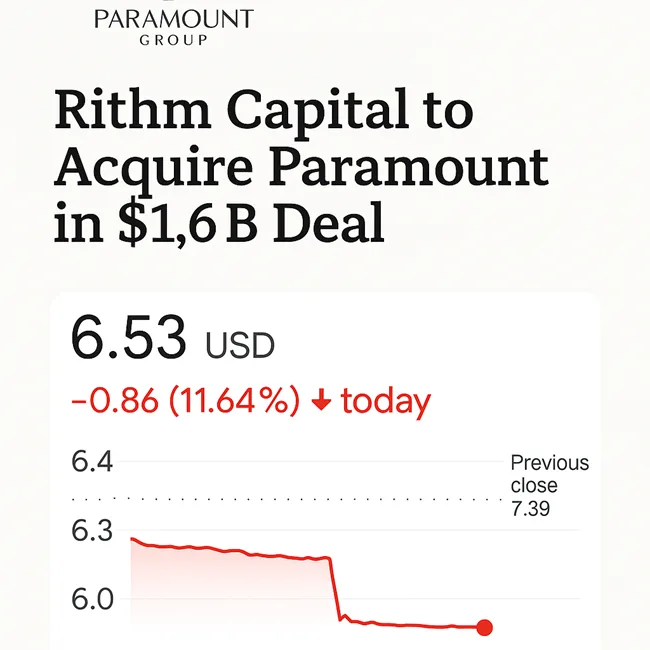

Rithm Capital Corp. (NYSE: RITM) announced that it has entered into a definitive agreement to acquire Paramount Group Inc. (NYSE: PGRE) for $1.6 billion in an all-cash transaction, marking one of the most significant office real estate takeovers of 2025. Paramount shareholders will receive $6.60 per fully diluted share, valuing the company’s 13.1 million square foot portfolio of Class A office space in New York City and San Francisco. Yet, despite the scale of the deal, Paramount’s stock price plunged more than 11 percent to $6.53 on September 17, compared with a previous close of $7.39. The sharp decline reveals the complicated dynamics of the office real estate sector and investor expectations that were not met by the agreed transaction terms.

The boards of both Rithm Capital and Paramount Group have unanimously approved the deal, which is expected to close in the fourth quarter of 2025, subject to shareholder and regulatory approvals. Rithm intends to fund the acquisition using a mix of cash reserves and balance sheet liquidity, supplemented by potential co-investment opportunities. For Rithm, the deal provides a springboard into large-scale ownership of high-quality urban office assets, while for Paramount shareholders, it offers certainty of value after years of trading at a discount to net asset value. However, the market reaction underscores that certainty does not always equal satisfaction.

Why did Paramount Group agree to a $6.60 per share deal and what does it mean for valuation?

Paramount Group has long been considered a pure-play New York and San Francisco office landlord, with trophy assets such as 1301 Avenue of the Americas and One Market Plaza. But the stock has traded at a persistent discount to book value, reflecting concerns over leasing fundamentals, hybrid work patterns, and the slow recovery of urban office demand. As of June 30, 2025, the company’s portfolio was 85.4 percent leased, down from levels above 90 percent before the pandemic.

The purchase price of $6.60 per share represents a modest premium to recent trading ranges, but many investors had anticipated a valuation closer to $7.50 or even $8.00, given the intrinsic worth of the assets. The reality of the lower buyout price left shareholders underwhelmed. The outcome reflects both the challenging economics of office real estate and the limited bargaining power Paramount had in a market where buyers are scarce. For investors who had held the stock in hopes of a stronger re-rating, the deal represents a compromise between immediate liquidity and long-term uncertainty.

How does the acquisition fit into Rithm Capital’s long-term commercial real estate strategy?

Rithm Capital has built its reputation as a global alternative asset manager focused on mortgage servicing rights, structured finance, and credit strategies. The acquisition of Paramount represents a deliberate pivot into direct ownership of commercial real estate at scale. Chief Executive Officer Michael Nierenberg described the acquisition as a generational opportunity to expand the firm’s owner-operator model and diversify its asset management platform.

By integrating Paramount’s operations into Rithm’s existing GreenBarn subsidiary, the company will inherit a seasoned management team and a portfolio of high-quality urban properties. This positions Rithm to pursue redevelopment opportunities, reposition buildings for new tenant demand, and leverage its financial scale to extract efficiencies. Analysts suggest that this deal marks the beginning of a more aggressive push by Rithm into physical real estate, adding depth to its existing asset-light businesses.

Why did Paramount’s stock price fall after the takeover announcement despite an all-cash offer?

The paradox of the announcement is that Paramount’s stock, rather than rising toward the deal price, fell sharply in trading. The reason lies in the gap between market expectations and the announced terms. In the weeks before the announcement, speculation of a potential sale had lifted Paramount’s stock above $7.00, as investors priced in the possibility of a premium closer to 20 percent. Once the definitive agreement revealed a price of only $6.60, those investors recalibrated, leading to an immediate sell-off.

This “deal disappointment discount” was amplified by broader skepticism about the office market. Many investors remain wary of office REITs, particularly those concentrated in San Francisco, where vacancy rates are still among the highest in the country. Even New York, with its diversified tenant base, continues to face elevated sublease availability. Against this backdrop, some funds chose to exit positions rather than hold for minimal upside until the transaction closes.

What does the Paramount transaction signal about the U.S. office REIT market in 2025?

The sale of Paramount to Rithm reflects a broader trend of consolidation in the office REIT space. With financing costs elevated and public valuations depressed, many REITs are vulnerable to acquisition by private capital and alternative asset managers. Paramount’s decision to sell at a modest valuation underscores the lack of liquidity and investor appetite in the public markets.

Historically, Manhattan office towers were considered blue-chip investments with resilient demand. But since the pandemic, hybrid work has fundamentally altered occupancy trends. Average Class A office occupancy across the United States remains in the low 80s, compared with pre-2020 levels above 90 percent. Landlords have been forced to offer concessions and tenant allowances, compressing margins and reducing dividend capacity.

In this environment, private managers like Brookfield, Blackstone, and now Rithm are selectively acquiring assets they believe can be repositioned or held for recovery. The Paramount deal signals that sellers are willing to take cash and exit rather than wait for an uncertain rebound in valuations.

How are analysts and institutional investors viewing Rithm Capital’s $1.6 billion office bet?

Market reaction among analysts has been divided. Some see Rithm’s move as a savvy countercyclical bet on high-quality office assets in markets that could recover if interest rates ease and leasing demand improves in 2026. The firm’s ability to finance the transaction without over-leveraging gives it flexibility, and the integration with GreenBarn may unlock operational synergies.

Others remain cautious, warning that San Francisco’s persistently high vacancies and New York’s slow absorption of space present meaningful risks. The risk-return trade-off hinges on whether Rithm can create value through redevelopment, sustainability retrofits, or mixed-use repositioning. Institutional flows suggest hedge funds have trimmed PGRE exposure, while long-only funds appear inclined to hold shares until the transaction closes, treating the stock as a quasi-bond set to pay out at $6.60.

What could Rithm Capital’s ownership mean for Paramount’s assets and employees?

For Rithm, the acquisition opens the door to reshaping Paramount’s portfolio with a focus on returns. Analysts expect Rithm to consider recycling non-core assets, investing in modernizing buildings, and potentially converting select properties into mixed-use formats. The firm’s capital flexibility allows for long-term positioning, which may benefit tenants seeking sustainable, amenity-rich office environments.

For Paramount’s employees and management, integration into a larger asset manager may bring changes in governance and strategy. Whereas REITs often prioritize dividend stability, Rithm’s model emphasizes capital appreciation and performance-based management. This cultural shift could reshape how assets are marketed, leased, and redeveloped in the coming years.

What is the investor sentiment and stock outlook after Paramount’s takeover announcement?

The immediate reaction to the deal demonstrates how investor sentiment often diverges from corporate strategy. On paper, the $1.6 billion cash acquisition provides certainty of value for Paramount shareholders. In practice, the lack of a stronger premium left the market underwhelmed. The stock’s drop to $6.53 highlights investor frustration, particularly among those who bought shares above $7.00 in anticipation of a more lucrative buyout.

For retail investors, the decision is now a straightforward calculation: sell into the market at current levels or hold through to closing for the guaranteed $6.60 payout. For institutional investors, the play is largely about arbitrage, with little incentive to accumulate beyond short-term strategies. Analysts categorize PGRE as a “hold” in the near term, with limited upside until deal completion.

For Rithm shareholders, the acquisition could be viewed as a diversification play that strengthens the company’s positioning in commercial real estate. The firm now stands alongside other alternative managers that are buying distressed or undervalued assets with a long-term view. If leasing markets stabilize and interest rates ease in 2026, Rithm could unlock significant value from the Paramount portfolio, validating its contrarian strategy. Until then, the market remains cautious, with the burden of proof on Rithm to demonstrate execution.

Share this:

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.