Why is Nuveen’s $1.3 billion first close of EPIC II seen as a strong signal for private infrastructure credit markets?

Nuveen, the investment manager owned by Teachers Insurance and Annuity Association of America (TIAA), has raised approximately $1.3 billion in the first close of its Energy & Power Infrastructure Credit Fund II (EPIC II). The capital, secured from a mix of global institutional investors, underlines the rising role of private credit as banks continue to scale back exposure to capital-intensive energy projects. The fund is designed to provide debt financing across both renewable energy and hydrocarbon-linked infrastructure, positioning Nuveen at the heart of the financing required for the ongoing global energy transition.

The close was anchored by TIAA and a leading Canadian pension fund, while nearly half of the commitments came from outside the United States, reflecting the global appetite for dollar-denominated, yield-focused private debt opportunities. For Nuveen, which has already deployed more than $13 billion across energy credit cycles, EPIC II represents a continuation of its strategy of structuring senior secured loans against hard assets and contracted cash flows.

How does Nuveen plan to deploy capital across renewable energy, storage, and midstream hydrocarbons under EPIC II?

EPIC II will primarily target senior debt instruments, including term loans and structured credit facilities, designed to finance energy projects that combine operational resilience with long-term revenue visibility. According to Don Dimitrievich, who heads Nuveen’s energy infrastructure credit team, investors are increasingly drawn to strategies that provide “resilient investments that can withstand volatile commodity cycles.”

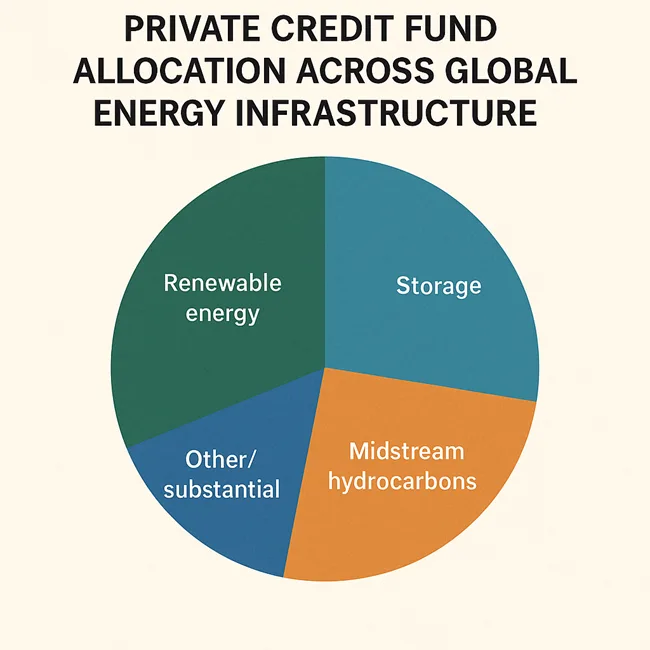

This approach means EPIC II is not a narrowly defined renewable-only vehicle. Instead, it balances exposure between renewable energy generation, grid-scale storage, and midstream hydrocarbon infrastructure such as pipelines and processing facilities. By combining both ends of the energy spectrum, the fund is designed to provide investors with stable, downside-protected cash flows while retaining exposure to energy transition-linked growth.

For borrowers, the fund offers an alternative source of capital at a time when traditional banks are constrained by tighter regulatory capital rules. For investors, the strategy delivers an opportunity to capture steady yields while aligning, at least partially, with sustainability goals.

Why is private credit becoming such a dominant force in energy and power financing compared to traditional banks?

The strong investor response to EPIC II reflects a structural trend. Private credit in infrastructure has been expanding rapidly as commercial banks retrench from long-dated, capital-heavy sectors. New regulatory requirements such as Basel IV, combined with higher risk-weighted capital costs, have reduced banks’ appetite for large project loans in oil, gas, and even renewables.

At the same time, institutional investors—particularly pension funds and insurers—have been searching for yield opportunities that sit between investment-grade bonds and private equity. Infrastructure credit, with its asset-backed nature and long-term contracted revenues, offers a sweet spot. The rise of funds like EPIC II suggests that private capital is increasingly stepping into the role once played by global banks in financing the backbone of the energy system.

With interest rates showing signs of stabilization, the appeal of predictable mid-to-high single-digit returns from secured private loans is strengthening further. For many institutions, this provides portfolio diversification without the volatility typically associated with energy equities.

What does Nuveen’s fund structure reveal about institutional appetite for energy transition financing in 2025?

The first close of EPIC II was notable not just for its size but for its cross-border investor participation. Nearly half of commitments came from outside the United States, indicating broad confidence in Nuveen’s ability to underwrite across energy sub-sectors. European and Canadian pension funds, in particular, have been early movers in allocating capital to infrastructure credit, viewing it as both a yield enhancer and a hedge against inflation.

Institutional sentiment has shifted toward blended strategies that do not exclude hydrocarbons outright but instead balance them with renewable and decarbonization-linked projects. This approach reflects the reality that energy systems will require both conventional and new forms of generation and transport during the transition. By marketing EPIC II as a fund capable of bridging that gap, Nuveen has tapped into a global pool of investors comfortable with pragmatic ESG-linked credit allocations.

How do analysts view Nuveen’s track record and its ability to mitigate risks in the current energy financing cycle?

Analysts broadly view Nuveen’s $13 billion track record across prior energy cycles as a critical factor in EPIC II’s success. Having deployed capital through periods of high volatility, including oil price collapses and renewable subsidy shifts, the firm has demonstrated an ability to protect downside while maintaining steady distributions. Institutional investors see this as proof of disciplined underwriting, particularly in an environment where project execution risks and regulatory uncertainties remain high.

Potential risks flagged by market observers include changing regulations around fossil-fuel lending, potential delays in renewable project interconnections, and geopolitical tensions that could affect cross-border capital flows. However, the diversified portfolio approach that Nuveen is pursuing—spanning renewables, storage, and midstream hydrocarbons—provides a degree of natural risk mitigation. Analysts also note that senior secured debt positions provide lenders with asset recourse, offering further layers of protection compared to equity exposure.

What broader implications does the success of EPIC II carry for energy project developers and the private credit market?

The fund’s strong first close carries significant implications for both project developers and the broader private credit ecosystem. For developers, it signals that private debt remains a robust financing channel even as bank lending tightens. This is particularly important in the U.S. market, where renewable developers often face delays in accessing tax credit financing, and in emerging markets where sovereign-backed guarantees are thin.

For the private credit sector, EPIC II is a validation of infrastructure debt as a scalable asset class. The success of this close may encourage other managers to launch similar vehicles, particularly those focused on the intersection of energy transition and stable cash flows. As institutional allocations to private credit rise globally, energy and power infrastructure are expected to capture a significant share of that inflow.

What is the long-term outlook for Nuveen’s EPIC II fund and private infrastructure credit strategies?

Looking ahead, analysts expect Nuveen to scale EPIC II well beyond its $1.3 billion first close, potentially targeting a final size significantly larger depending on market conditions and project pipelines. Given the scale of capital required for energy transition infrastructure—estimated in the trillions globally over the coming decades—funds of this type are positioned to play an essential role.

The long-term outlook suggests that infrastructure credit strategies will increasingly complement equity in financing the transition. For investors, this provides exposure to critical energy projects without the volatility of commodity-linked equities. For developers, it offers a predictable source of capital at a time when public debt markets are often inaccessible or too expensive. If successful, Nuveen’s EPIC II could help set a new benchmark for blended, cross-border private credit allocations in energy finance.

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.

{kind=link}