Ithaca Energy PLC (LON: ITH) recorded a sharp gain of 2.41 percent on 20 November 2025, with shares rising to 233.50 GBX during the trading day, up from a previous close of 228.00 GBX. This price movement extends the stock’s five-day advance to 3.55 percent, fuelled by a combination of strong third-quarter results and the announcement of a strategic farm-in agreement with Shell UK covering the Tobermory gas discovery. The transaction marks another expansionary step in the company’s West of Shetland growth strategy and adds to the series of portfolio enhancements Ithaca Energy has executed in 2025 through both organic and inorganic means.

Investor sentiment appears to be responding not only to Ithaca Energy’s earnings strength and cash generation capabilities but also to the reaffirmed full-year dividend guidance and the acceleration of its second interim dividend. Market observers see these signals as indications that Ithaca Energy is balancing aggressive upstream expansion with disciplined capital returns, placing the United Kingdom-focused energy operator in a stronger position as it transitions into 2026.

How has Ithaca Energy stock performed this week and what is supporting the rally?

Shares in Ithaca Energy rose to 233.50 GBX by 15:28 GMT on 20 November, maintaining their position close to the session’s high of 234.00 GBX. Over the five-day trading window, the stock appreciated by 8.00 GBX, or 3.55 percent, as trading volumes and investor interest increased following the company’s November 19 results release and strategic update. The stock’s upward momentum is occurring within the context of improved operational visibility, cash flow certainty, and enhanced resource positioning through key M&A activity. This combination of organic production growth and strategic asset consolidation is contributing to improved investor confidence in Ithaca Energy’s medium-term roadmap.

On a valuation basis, Ithaca Energy continues to attract attention given its dividend yield of 7.87 percent and a market capitalization of approximately GBP 3.85 billion. The stock remains well off its 52-week high of 242.50 GBX but has more than doubled from its 52-week low of 98.80 GBX, reflecting broad-based gains driven by Eni UK asset integration and production ramp-up efforts throughout the year.

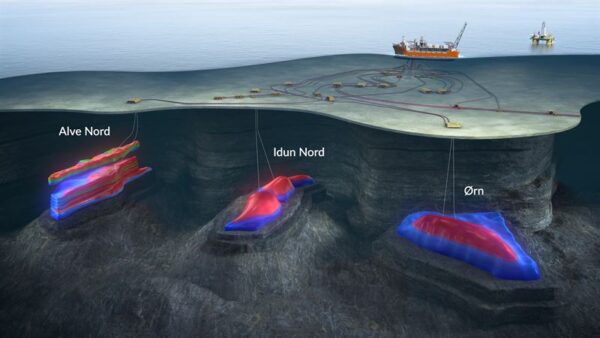

What are the strategic details of the Tobermory farm-in deal?

The Tobermory farm-in, announced on 19 November 2025, grants Ithaca Energy a 50 percent working interest in licences P2629 and P2630 in the West of Shetland basin. Shell UK will retain the remaining 50 percent interest and will continue to serve as operator. The licences include the Tobermory gas discovery, which sits adjacent to Ithaca Energy’s Tornado development, where the group also has a 50 percent stake in partnership with Shell. The Tobermory farm-in is being positioned by Ithaca Energy as a strategic enabler of future upstream synergies across its West of Shetland gas portfolio, particularly as it seeks to establish a more integrated gas hub in the area.

Executive Chairman Yaniv Friedman described the deal as a continuation of the company’s strategic partnership with Shell and a further demonstration of the importance of the West of Shetland basin to Ithaca Energy’s long-term growth plans. He noted that the company’s existing investments in the Rosebank, Cambo, and Tornado developments, when combined with the Tobermory asset, collectively support the United Kingdom’s energy security objectives while creating supply chain opportunities and long-term value for stakeholders.

The timing of the farm-in also aligns with other major operational milestones in the region. For example, the Rosebank development continues to progress on schedule, with subsea installations completed during Q3 and Floating Production Storage and Offloading (FPSO) vessel refurbishment advancing toward its Q1 2026 sail-away. Drilling activities are expected to commence in early 2026, while final investment decisions for both Cambo and Tornado are under active consideration subject to fiscal and regulatory conditions.

How did Ithaca Energy perform in Q3 2025 across financial and operational metrics?

Ithaca Energy’s Q3 2025 results marked a significant inflection point in terms of scale, profitability, and production efficiency. Year-to-date average production reached 114,900 barrels of oil equivalent per day, more than doubling the 52,500 barrels per day reported for the same period in 2024. This output level came despite heavy turnaround activity during the summer, particularly involving the Captain field, which extended its shutdown to accommodate further environmental and performance upgrades. The company also flagged that production was trending toward the lower end of its full-year guidance range of 119,000 to 125,000 barrels per day, due in part to the delayed startup of three high-production wells now expected to come online in December 2025.

Adjusted EBITDAX for the year-to-date period rose to $1.5 billion, up from $758.5 million in the same period last year. Operating costs were also materially reduced to $19.1 per barrel, compared to $28.9 per barrel in 2024, reflecting improved portfolio quality and the impact of the Eni UK asset integration. Profit before tax came in at $668.1 million for the nine-month period, though the company reported a year-to-date loss of $119.1 million due to a one-off, non-cash deferred tax charge of $327.6 million tied to the extension of the Energy Profits Levy to March 2030.

From a cash flow perspective, Ithaca Energy generated $1.28 billion in net operating cash flow for the year through September. As of the end of Q3, available liquidity stood at $1.7 billion, supported by a successful €450 million bond issuance and a $300 million upsizing of the company’s reserves-based lending facility. This translated into a conservative leverage ratio of 0.50x and an adjusted net debt position of $1.06 billion, positioning the company well to pursue future growth opportunities and strategic investments.

Which factors will shape Ithaca Energy’s dividend capacity, capital allocation priorities, and acquisition strategy as it scales its North Sea portfolio?

Ithaca Energy confirmed that its second interim dividend of $133 million, or $0.0804 per share, will be paid on 18 December 2025. This follows a first interim dividend of $167 million paid in September, taking total cash distributions declared for the year to $500 million. The group reaffirmed its full-year dividend guidance at this level, with the final tranche expected to be declared alongside full-year results in March 2026. The dividend strategy is underpinned by robust free cash flow generation, a disciplined cost structure, and enhanced portfolio cash margins.

In addition to the Tobermory farm-in, the group has executed a number of strategic acquisitions in 2025. These include the acquisition of JAPEX UK in July, which increased Ithaca Energy’s stake in the Seagull field from 35 percent to 50 percent, and the acquisition of a further 46.25 percent interest in the Cygnus field from Spirit Energy, bringing its total stake to 85 percent. These deals added a combined 18,000 barrels per day of pro forma production and were executed at what analysts view as attractive terms based on cash flow potential and asset maturity.

On the organic investment front, the company sanctioned additional well activity at Judy East Flank and Cygnus, while continuing to progress major development initiatives across its portfolio. The startup of three high-output wells in December, combined with successful integration of the Eni UK assets and new investment at key fields, is expected to support a raised Q4 exit rate of 145,000 barrels per day.

Which institutional sentiment trends, regulatory triggers, and operational milestones will investors monitor to assess Ithaca Energy’s 2026 outlook?

Analysts covering Ithaca Energy believe the stock’s recent momentum is being driven by a combination of operational discipline, predictable capital returns, and an expanding reserve and production base. The Tobermory farm-in, in particular, signals further potential for synergy-driven gas development in the West of Shetland, with Shell UK continuing to serve as a key partner. Investors are likely to watch closely for execution milestones tied to Rosebank and Cambo, clarity on United Kingdom fiscal terms for offshore investment, and continued adherence to cost control targets across the portfolio.

The stock’s five-day rally, reaching 233.50 GBX on 20 November, comes amid broader market interest in energy stocks with stable dividend profiles and long-life assets. Ithaca Energy’s yield, balance sheet strength, and production growth trajectory continue to make it one of the more closely watched energy plays on the London Stock Exchange heading into 2026.

What are the most important takeaways from Ithaca Energy’s Q3 update and Tobermory farm-in announcement?

- Ithaca Energy PLC (LON: ITH) shares climbed to 233.50 GBX on 20 November 2025, marking a 2.41 percent gain for the day and a 3.55 percent increase over the past five trading sessions.

- The stock rally followed the announcement of a 50 percent farm-in to Shell UK’s Tobermory gas discovery in the West of Shetland basin, solidifying Ithaca Energy’s partnership with Shell and reinforcing its regional gas hub strategy.

- The Tobermory farm-in complements Ithaca Energy’s existing 50/50 stake in the Tornado field and aligns with broader development plans at Cambo and Rosebank, as the company prepares for a 2026–2027 production timeline.

- Third-quarter results revealed a year-to-date average production of 114,900 barrels of oil equivalent per day, more than doubling from 52,500 barrels in 2024, despite a heavy summer turnaround schedule.

- Adjusted EBITDAX surged to $1.5 billion year-to-date, up from $758.5 million the year prior, while operating costs fell to $19.1 per barrel, driven by the integration of Eni UK assets and a more efficient portfolio mix.

- Net cash flow from operations hit $1.28 billion, supporting a strong liquidity position of $1.7 billion and a low leverage ratio of 0.50x as of Q3 2025.

- Ithaca Energy declared a $133 million second interim dividend, taking 2025 cash distributions to $500 million and reaffirming its full-year dividend guidance ahead of final results in March 2026.

- Strategic M&A moves included the full acquisition of JAPEX UK and a 46.25 percent stake in the Cygnus field from Spirit Energy, adding approximately 18,000 barrels of daily production.

- Key 2026 investor watchpoints include timely well startups in December, progress on Cambo’s final investment decision, fiscal clarity from the UK government, and delivery of the Rosebank FPSO by early Q1 2026.

- Analysts see Ithaca Energy’s capital return strategy, operational consistency, and gas-heavy growth positioning as reasons for growing institutional confidence in the stock.

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.