Why are Nuveen, Blackstone and Brookfield leading the private credit charge in energy and infrastructure?

Nuveen, Blackstone, and Brookfield are spearheading a transformative trend in energy finance, using private credit to address a funding void left by traditional banks retreating from capital-intensive infrastructure projects. Nuveen recently secured $1.3 billion for its Energy & Power Infrastructure Credit Fund II (EPIC II), reflecting global institutional interest in senior secured lending across renewables, storage, and hydrocarbons. This follows Blackstone’s record $7.1 billion Green Private Credit Fund III (BGREEN III) and its $5.6 billion Blackstone Energy Transition Partners IV (BETP IV), both fully subscribed at their hard caps. Meanwhile, Brookfield raised $14 billion in credit strategies in early 2025, including $1.5 billion for renewable power and transition strategies and one of its largest ever global transition funds.

The scale of these raises highlights how private capital is increasingly becoming the backbone of energy project financing. Each of these funds reflects a wider investor shift: a willingness to embrace secured credit rather than equity exposure in an effort to capture stable, yield-driven returns.

What is driving institutional capital toward private credit in energy transition financing?

Institutional investors such as pension funds and insurance companies are steadily increasing allocations to private credit due to its steady, contract-backed returns and asset-based security. Stricter capital requirements under Basel IV, combined with banks’ reduced risk appetite for long-dated loans, have sharply cut traditional bank lending into energy infrastructure.

This retreat has opened the door for funds like Nuveen’s EPIC II, Blackstone’s BGREEN III, and Brookfield’s transition vehicles to provide structured lending across the sector. Market data suggests that mega-funds above $5 billion accounted for nearly half of all infrastructure fundraising in 2024. These large platforms, concentrated among a handful of global managers, are dominating the space.

The attraction is clear: secured debt tied to hard assets and long-term cash flow contracts delivers predictable income. For investors balancing liabilities, private credit offers diversification without the volatility of public equities or high-yield bonds. For borrowers, it represents a lifeline as capital-intensive projects demand financing solutions outside the shrinking balance sheets of commercial banks.

How have Blackstone’s energy transition funds performed compared to Nuveen’s new credit strategy?

Blackstone’s BGREEN III raised $7.1 billion, the largest private credit energy transition fund to date. The fund invests across renewable generation, infrastructure, and energy transition opportunities. It closed at its hard cap, underscoring surging demand for yield-oriented ESG-linked strategies. Following this, Blackstone closed BETP IV at $5.6 billion, also at its hard cap. Together, these two funds illustrate the enormous appetite for private credit within the energy transition.

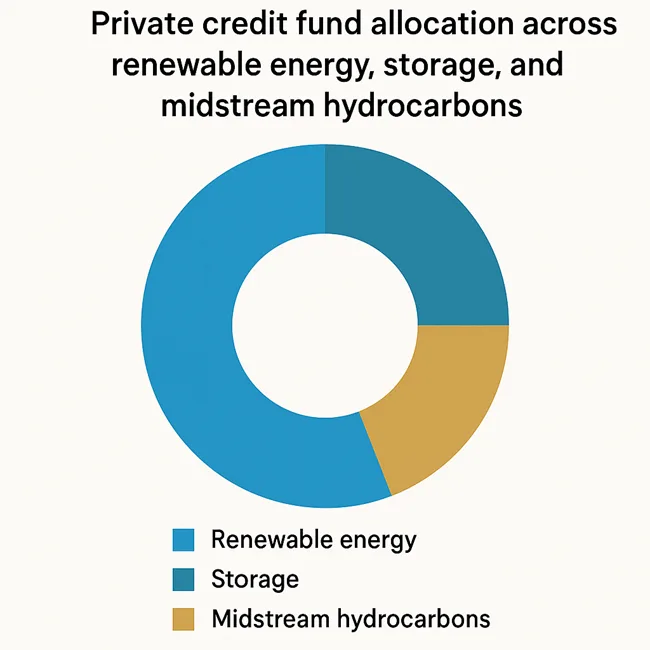

Nuveen’s EPIC II complements this trend but with a slightly different mix. By combining renewables, grid-scale storage, and midstream hydrocarbons, Nuveen positions itself as a diversified lender across both clean energy growth and conventional energy stability. This diversification appeals to institutions unwilling to commit solely to renewable-only credit but still keen on sustainability credentials.

Taken together, the strategies of Blackstone and Nuveen reveal a convergence: institutional investors want exposure to energy transition themes, but they also demand resilience in their portfolios. Private credit provides the structured, senior-secured model to achieve both.

What strategic advantage does Brookfield bring in private credit and infrastructure fundraising?

Brookfield brings scale, diversification, and an unmatched global footprint to infrastructure credit. In the first quarter of 2025, it raised $14 billion across credit, $1.5 billion in renewable and transition strategies, and $1.7 billion in infrastructure vehicles including its “supercore” strategy. Its second global transition fund, one of the largest in the market, is still on track for a final close.

Brookfield’s advantage lies in its ability to blend credit with direct equity ownership across utilities, renewable platforms, and infrastructure concessions. This integrated model enables Brookfield to deploy capital in multiple layers of the capital structure. For institutions, this means access to a manager that can underwrite across cycles, across geographies, and across technologies.

The firm’s size and reputation also mitigate concentration risk, a common challenge in private credit. Brookfield can deploy across dozens of countries, making it more resilient to regional policy shifts or market downturns than single-market lenders.

What does this surge in private credit mean for energy project developers?

For energy project developers, the rise of private credit funds is a critical development. With banks constrained and public debt markets often too volatile, developers now have a robust alternative financing channel. Funds like Nuveen’s EPIC II or Blackstone’s BGREEN III offer predictable, structured debt capital that allows projects to move forward.

This is particularly important in renewable energy, where tax credit financing or state-backed guarantees may take time to secure. In midstream and conventional energy infrastructure, private credit provides long-term funding without the cyclicality of equity markets.

Deals like Blackstone’s multi-billion-dollar structured financing of pipelines through senior-rated tranches show how these vehicles can preserve investment-grade credit profiles while ensuring developers have the liquidity needed to deliver large projects. For developers, the message is clear: private credit is no longer a niche—it is central to the capital stack of the energy sector.

What are the risks and thresholds in scaling energy transition credit strategies?

Despite investor enthusiasm, several risks remain. Regulatory uncertainty is the most immediate. Changes in fossil fuel lending policy could affect funds with exposure to hydrocarbons. Project execution delays in renewables—caused by supply chain issues, interconnection backlogs, or permitting hurdles—can undermine repayment schedules.

Geographic concentration is another challenge. Managers that lean heavily into single regions risk being overexposed to local policy reversals. Brookfield’s global scale reduces this, but mid-sized funds remain more vulnerable.

Analysts also caution that transparency and governance will be increasingly important. Some fund managers have faced scrutiny over tax structures or fee arrangements. For institutions deploying billions into private credit, clearer reporting will be essential to maintain confidence.

That said, the structural protections of senior secured lending, combined with diversification across renewables and hydrocarbons, provide a strong cushion. Funds like EPIC II, BGREEN III, and Brookfield’s transition platforms are deliberately designed to withstand shocks, whether from commodity prices or regulatory swings.

What is the outlook for private credit in energy infrastructure over the next decade?

Looking ahead, private credit is expected to remain a central pillar of energy and infrastructure financing. With trillions required to fund the global energy transition, public debt markets and banks cannot meet the demand alone. Private credit, with its blend of predictable returns and ESG alignment, is well placed to fill the gap.

Nuveen is expected to scale EPIC II significantly beyond its initial $1.3 billion first close. Blackstone will continue deploying BGREEN III and BETP IV into energy transition projects, while Brookfield’s pipeline suggests more mega-fund closes ahead.

For investors, private credit offers stability, diversification, and alignment with long-term transition goals. For developers, it offers an increasingly indispensable financing option. For the energy sector, it signals that the backbone of capital formation is shifting—from banks and public markets to private institutional credit.

Discover more from Business-News-Today.com

Subscribe to get the latest posts sent to your email.